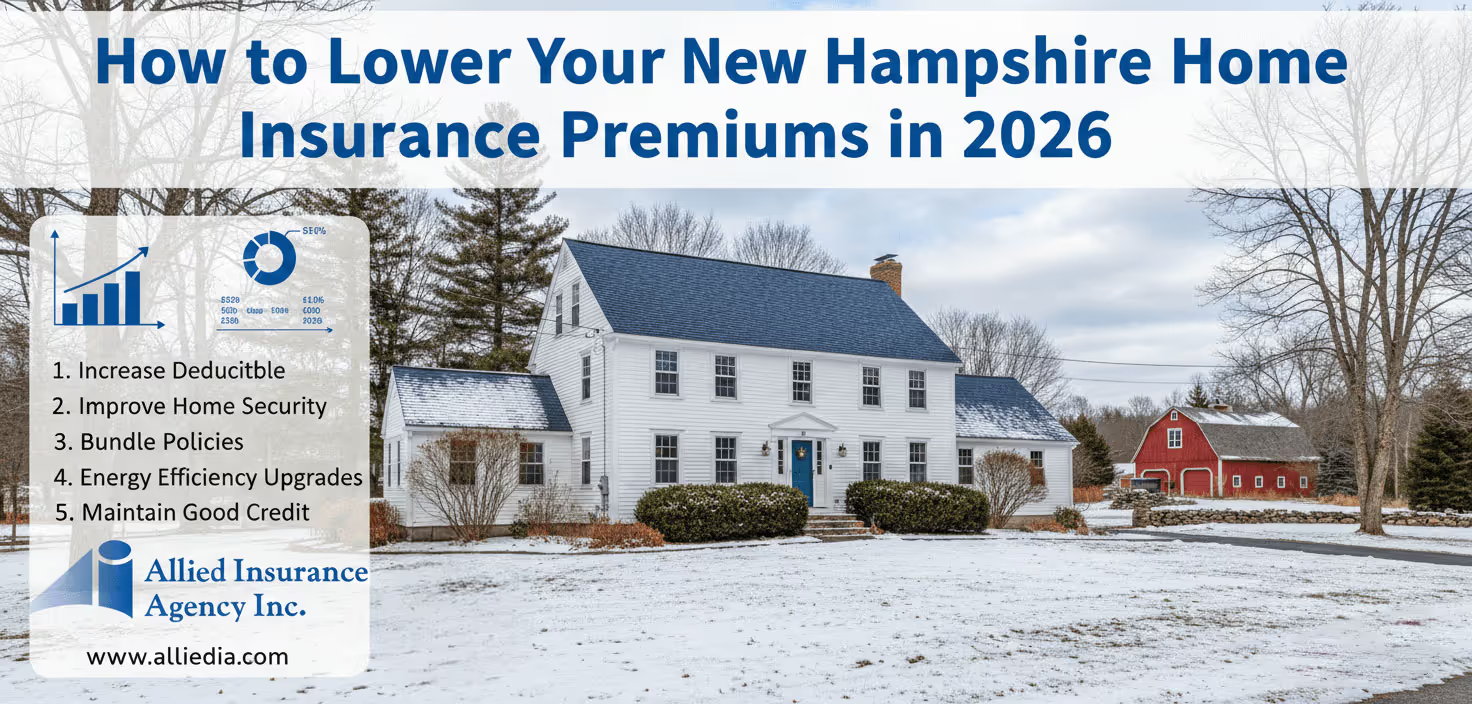

How to Lower Your New Hampshire Home Insurance Premiums in 2026!

This short guide helps homeowners in New Hampshire understand smart, practical steps to reduce policy costs in 2026 without creating coverage gaps.

The agency perspective is clear and local. It notes that annual rates in the state commonly range from about $953 to $1,185, well below the U.S. average. That gap creates room to improve value while staying budget-conscious.

Readers will learn how insurers evaluate risk factors like claims history, credit, location, rebuilding cost, and deductibles. The article frames four actionable levers: policy design, discounts, targeted home improvements, and shopping multiple quotes.

The guide also touches on local concerns for Concord, Bow, and Hooksett, such as winter losses and riverside flood exposure. It defines premium in plain language and shows how choices about maintenance and protection affect rates.

Key Takeaways

- 2026 pricing in the state is often below the national average, so aim for smarter value, not just the cheapest quote.

- Insurers focus on claims, credit, rebuild cost, and deductibles when setting costs.

- Actionable levers include policy choices, discounts, home upgrades, and comparing multiple quotes.

- Local risks like winter weather and river flooding matter for Concord, Bow, and Hooksett residents.

- An independent agent helps interpret coverage and avoid gaps while seeking savings.

New Hampshire home insurance in 2026: what premiums look like and why rates stay competitive

This year, housing protection in the state often comes at a clearer cost advantage versus the U.S. average. Annual ranges in 2026 commonly sit between $953 and $1,185, versus nationwide averages near $1,754 to $2,110. That roughly 44% to 46% gap gives policyholders room to improve coverage or add endorsements while staying within budget.

How pricing compares to the national average

The difference in price allows many owners to choose stronger limits or broader property protections without a big jump in cost. Careful comparison can reveal real value beyond sticker rates.

Why local risk factors still matter

Lower state averages do not remove exposure. Winter weather, wind events, and water damage remain common New England loss drivers that affect claim frequency and pricing.

What competition among 30+ providers means

With more than thirty companies active, insurers vary in underwriting, credits for upgrades, and claim service. That competition helps buyers shop for both price and long term policy value.

How insurers set homeowners insurance rates in New Hampshire

A range of factors explain why two similar residences can receive very different quotes in the same town. Insurers combine personal data, property details, and local conditions to estimate future risk and set a fair price.

Credit-based scores and the impact of stronger credit

Credit-based insurance scores are allowed in the state and often influence pricing. Better credit histories typically lead to lower cost because they correlate with fewer claims over years.

Improving credit gradually can produce measurable savings when policies renew.

Claims history and filing effects

Frequent claims can raise rates or narrow renewal options. Multiple small claims within a few years may trigger significant increases or higher scrutiny at renewal.

Dwelling value, rebuild cost, and construction trends

Market value and rebuild cost differ. Cover the dwelling to match rebuild estimates so rising construction and labor costs do not leave gaps.

Deductibles, liability, and out-of-pocket tradeoffs

- Higher deductibles often reduce the annual cost by about 10% to 15% for common increases.

- Choose liability limits to match asset exposure; higher limits protect against growing claim amounts.

- Keep an emergency fund to cover larger deductibles when claims occur.

Location-based rating across Concord, Bow, and Hooksett

Local factors such as fire protection class, response times, and proximity to rivers affect rates. Two homes in Concord can differ from Bow or Hooksett because of these local risks.

lower home insurance premiums new hampshire with smarter policy design

Smart policy design starts with matching coverage to real rebuilding needs, not sale price. An independent agent helps verify limits, valuation methods, and deductible choices so protection remains solid while cost becomes more efficient.

Right-size dwelling coverage to rebuild cost, not market price

Dwelling coverage should reflect the cost to rebuild the structure after a loss. Market value often includes land and local demand, which do not affect rebuild expenses in Concord, Bow, or Hooksett.

Choose replacement cost vs actual cash value for personal property

Replacement cost pays to replace items without depreciation. Actual cash value reduces payouts for older items. For electronics and furniture, replacement cost often gives better long term value despite modest policy cost differences.

Adjust deductibles strategically and keep an emergency fund ready

Raising a deductible can reduce the annual premium but increases out-of-pocket risk. Maintain an emergency fund sized for the deductible so a claim does not cause a financial shock.

Review liability coverage and consider higher limits

Liability limits protect assets if a serious injury occurs on the property. Increasing liability is often cost effective when compared to potential claim exposure in today’s legal environment.

An independent agency can compare multiple policies and verify rebuild-cost inputs and personal property valuation to optimize protection and value.

Contact Allied Insurance Agency in Bow, N.H. for a free home insurance quote.

Discounts and savings New Hampshire homeowners can stack without cutting protection

Savings add up when policyholders combine the right credits and modern loss-prevention systems. Stacking discounts is effective when coverage remains correctly designed first.

Bundle strategically

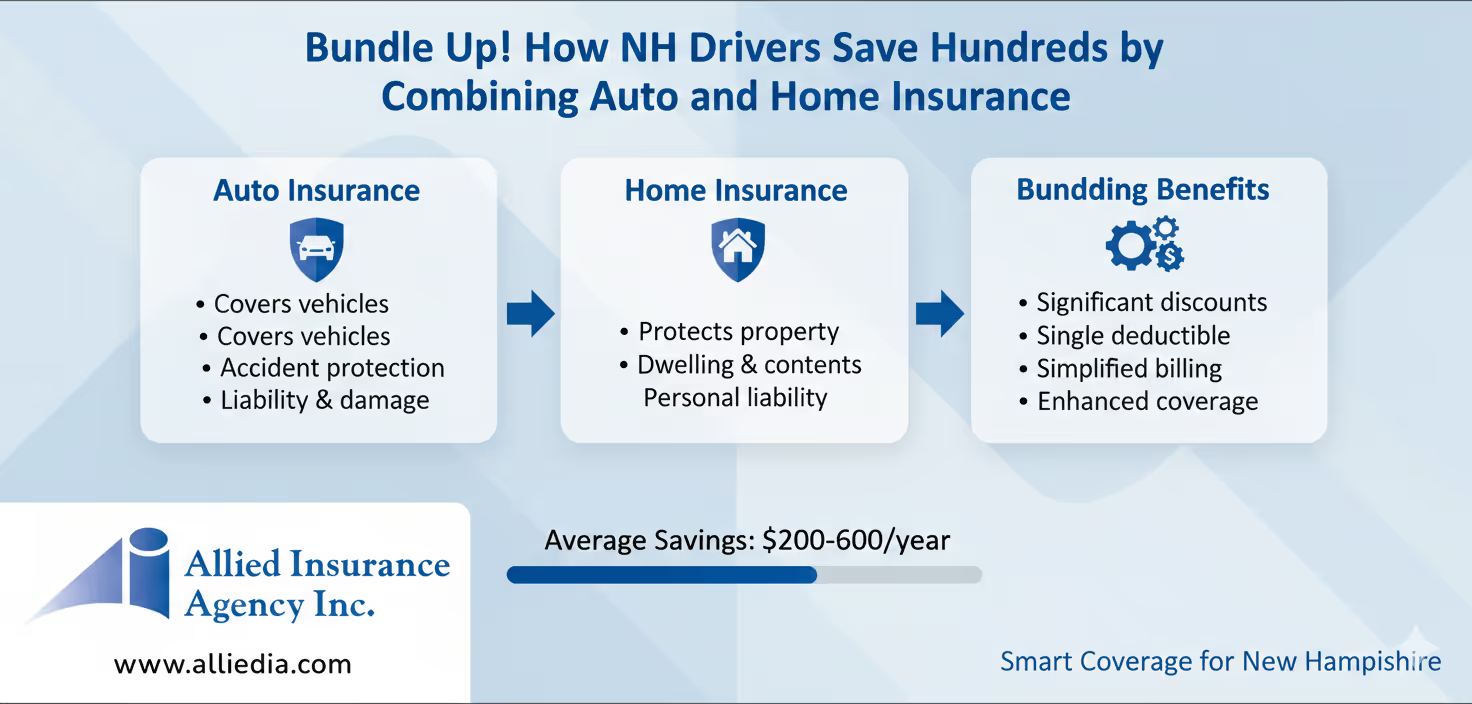

Bundling home and auto policies to target 10% to 25% savings

Bundling home and auto often yields the largest single discount, typically between 10% and 25%. Confirm that the bundled quote truly saves versus two separate policies before switching.

Security and risk-reduction credits

Home security and fire protection upgrades that can qualify for 2% to 15% discounts

Monitored alarm systems, hard-wired smoke detectors, and sprinkler or fire suppression upgrades commonly earn 2% to 15% discounts depending on underwriting rules.

Smart sensors, water shutoff devices, and freeze alerts to reduce water damage risk

Water-leak sensors, automatic shutoff valves, and freeze alerts reduce the likelihood of costly water losses. Insurers may offer credits for these systems because they cut claim frequency.

Payment, paperless, and claims-free options that can lower overall insurance costs

Paperless billing, automatic payments, and a clean claims history can produce small discounts and steadier renewal costs. Avoiding minor claims preserves eligibility for many credits.

- Stack discounts ethically after verifying coverage limits and valuation methods.

- Remember flood protection is separate from standard coverage, especially near rivers or low-lying areas.

- An independent agent can confirm which discounts apply in Concord, Bow, or Hooksett and ensure savings do not trade away protection.

Contact Allied Insurance Agency in Bow, N.H. for a free home insurance quote.

Home improvements that can lower premiums and reduce claim risk in New England weather

Practical upgrades reduce the chance of a costly claim and make a residence easier to repair after a storm.

Roof, siding, and storm-resistant construction

Wind-rated roofing, impact-resistant siding, and proper flashing cut water intrusion after ice and wind events. For properties in Concord, Bow, and Hooksett, replacing older shingles and reinforcing eaves protects the structure and lowers the likelihood of damage.

Electrical, plumbing, and HVAC updates

Modern electrical panels and updated plumbing reduce fire and water exposure from failing systems. Upgrading HVAC components and appliances limits breakdowns that cause water losses and fire starts over the years.

Ice dam prevention, sump pumps, and backups

Attic insulation and ventilation minimize ice dams. Sump pumps with battery backup and exterior drainage reduce basement flooding and long term property harm. These measures cut claim frequency and ease recovery after events.

- Document improvements with receipts and photos.

- Request a policy review so the insurer notes upgraded materials and systems.

- Fewer losses over time help maintain claims-free status and preserve better pricing and protection value.

Quote shopping in Concord, Bow, and Hooksett: how to compare policies beyond price

Comparing a quote means checking what pays after a loss, not just the shown price. Homeowners should match limits, exceptions, and service levels across companies.

What to verify in every quote

Ask for clear answers on deductible type, dwelling limit basis, and whether personal property uses replacement cost or actual cash value.

Confirm water backup options and key exclusions that can surprise homeowners during a claim.

Endorsements and claims handling

Endorsements often turn a basic policy into a better fit. Compare the same endorsements across insurers so you measure true coverage.

Evaluate each insurer for adjuster availability and how they handle claims after storms.

Flood risk and separate coverage

Properties near rivers or low ground face flood exposure. Flood protection is typically separate from standard policies.

Do not assume river overflow or surface water is covered. Seek a dedicated flood quote when risk exists.

Fire protection class and neighborhood rates

Fire protection class, hydrant distance, and response times change rates by neighborhood. A house a few miles away can show different rates for that reason.

An independent agency helps compare insurers and translates insurance costs into real-world protection outcomes.

Contact Allied Insurance Agency in Bow, N.H. for a free home insurance quote.

Conclusion

A focused approach to coverage and risk reduction helps Granite State owners keep value and control costs.

New Hampshire rates often sit well below national averages, so homeowners can keep strong coverage while optimizing price through thoughtful policy design, strategic deductibles, and targeted risk improvements. Flood protection is typically separate and should be quoted where river or surface-water risk exists.

Credit and claims behavior shape long term pricing, so routine maintenance and careful claim choices matter. Stack discounts only after ensuring limits, endorsements, and rebuild estimates match real needs.

For a practical checklist and to spot extra fees, see this hidden fees guide.

Contact Allied Insurance Agency in Bow, N.H. for a free home insurance quote.