10 Hidden Fees in New Hampshire Home Insurance Policies

This concise guide explains what residents should expect when a policy quote grows into a final bill. It focuses on how line items beyond the base premium change the total cost for Concord, Bow, and Hooksett homeowners.

Insurers here weigh credit, roof age, and claims history heavily. Many require roofs under 20 years and may cancel mid-term after an inspection if a roof is poor. This creates add-ons that show up after binding.

Contact Allied Insurance Agency for a free N.H. home insurance quote.

Key Takeaways

- Understand the difference between listed premiums and the total cost with add-ons.

- Roof condition, credit, and prior claims often trigger surcharges for residents.

- Ask for line‑item explanations before binding to avoid surprises.

- Independent agents help compare options and clarify policy language.

- Simple maintenance and billing choices can lower what homeowners actually pay.

Why hidden fees matter for New Hampshire homeowners

This year’s changes in claims severity and materials pricing have real effects on what residents pay. New Hampshire’s average homeowners premium in 2024 sits near $1,002, well below the national average. Yet local market shifts push up insurance rates and add non‑premium costs that raise the final bill.

Inflation and higher construction labor costs in Concord have increased repair expenses. That drives carriers to add underwriting surcharges or adjust billing. In Hooksett, proximity to the Merrimack River raises flood and storm risk, which can lead to special deductibles or surcharges even when a quoted premium looks low.

Older roofs in Bow and many Concord neighborhoods trigger inspections and reinspection charges tied to underwriting requirements. These are separate from the base premium and can change the out‑the‑door amount for any given policy.

- Understand how local rebuilding costs and weather trends feed both premiums and extra charges.

- Ask an independent agency to clarify how each factor affects your total costs.

- Compare quotes at the micro‑area level — state averages can mask neighborhood differences.

hidden fees home insurance new hampshire: what to watch for before you buy

Before you sign, many line items can raise the total you owe at binding or renewal. An experienced independent agent recommends reviewing the final invoice closely so there are no surprises.

Policy issuance and service charges that appear at binding or renewal

Carriers may add administrative or issuance charges when they bind a policy or process a renewal. These can push the amount due above the quoted premiums even when coverage stays the same.

Payment plan and installment fees with monthly billing

Monthly plans often carry per‑payment processing costs. Over a year, those charges can exceed the savings of paying monthly versus annual or semiannual billing.

Inspection and reinspection costs tied to roof or update requirements

Many New England insurers require roofs under 20 years. If an inspection finds work is needed, reinspections and verification costs can be billed to the policyholder.

Endorsement add‑ons that inflate premiums without notice

Optional coverages such as water backup or ordinance upgrades are sometimes included by default. Ask for a line‑by‑line disclosure to remove nonessential endorsements.

High‑risk surcharges related to claims, credit, or prior cancellations

Poor credit or recent claims can raise premiums sharply in New Hampshire. These surcharges stack on the base rate and change renewal totals.

- Ask for full fee disclosures in writing before binding.

- Compare billing cadences to quantify annual differences.

- Perform a line‑by‑line policy review to remove unneeded add‑ons.

- Contact Allied Insurance Agency for a free insurance quote.

Fee triggers unique to New Hampshire homes

River-adjacent underwriting has tightened in areas like Concord and Hooksett after stronger storm seasons. Properties along the Merrimack can face separate wind or named-storm deductibles, extra inspection requirements, and underwriting surcharges that often surface during review rather than on initial quotes. Contact Allied Insurance Agency for a free N.H. home insurance quote.

Roof age and material thresholds

Roof age is a common trigger. When a roof nears the insurer threshold, inspections, reinspections, or mid-term actions may follow. Material choice matters: local data shows roughly a $74 spread in premiums by roof type, so composition can reduce or raise surcharges.

Older construction and required upgrades

Historic neighborhoods in Bow and Concord often require electrical, plumbing, or heating updates before full coverage is approved. Photographic verification or in-person inspections are common and can generate verification costs billed to the homeowner.

- Request a written list of contingent charges before binding.

- Document recent repairs with invoices and photos to limit reinspection.

- Discuss replacement schedules for roofs and systems to preserve favorable coverage.

Cost impact: how small fees raise your total insurance costs

What looks like a fair premium on paper can climb once service, processing, and verification items are tacked on. The quoted rate is only the starting point; the final statement often adds administrative, installment, inspection, and endorsement amounts that change the total cost.

From base premium to out-the-door price in New Hampshire

Data shows the scale: the 2024 average premium in New Hampshire is about $1,002 versus $2,423 nationally. Service and processing line items can add several hundred dollars to that figure, depending on billing cadence and required verifications.

Credit score and claims history as hidden cost multipliers

Credit can swing rates dramatically. In this state, poor credit averages about $2,133 while excellent credit is near $803 — roughly a $1,330 difference for similar coverage. Likewise, one claim in five years raises the average to about $1,275; two claims push it to roughly $1,552, compared with a claim‑free $1,002.

Construction and repair inflation pushing coverage and fees higher

Rising material and labor costs, especially in Concord, increase rebuilding estimates. Higher rebuild values lift premiums and associated verification or endorsement charges when carriers reassess replacement cost figures.

- Break down the final invoice to see how a base premium becomes an out‑the‑door price.

- Compare billing schedules to quantify annual cost differences from installment processing.

- Ask for a comprehensive fee schedule and document recent upgrades to limit reinspection charges.

- Contact Allied Insurance Agency for a free insurance quote.

Contact Allied Insurance Agency for a free home insurance quote.

Ten fee categories New Hampshire residents should scrutinize

A clear review of common charge categories prevents surprises at binding or renewal. Below is a professional checklist from an independent agency tailored to New Hampshire realities. Use it to spot adjustments that commonly appear after a quote.

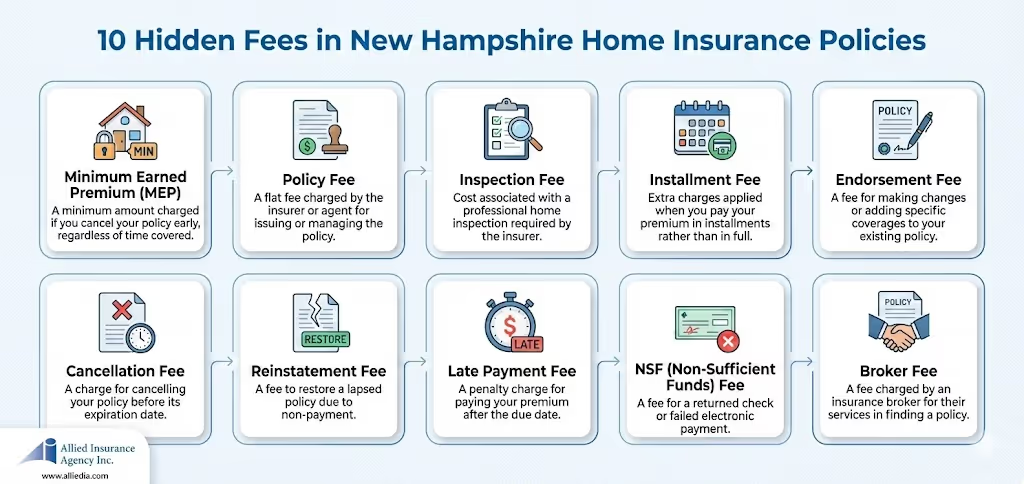

Minimum earned premium and short‑rate cancellation penalties

What it means: Canceling mid‑term can leave the policyholder responsible for a prorated, nonrefundable portion of the premium plus a penalty. Review the policy's earned premium table before switching providers.

Inspection, photo, or verification charges after binding

Insurers may bill for roof, heating, or safety verifications requested after binding. Document repairs with invoices and photos to reduce reinspection needs.

Payment processing and third‑party transaction fees

Card or third‑party payments sometimes add per‑transaction costs. Choose bank draft or in‑agency payments to avoid extra charges.

- Endorsements: Valuables, water backup, and ordinance coverage can raise premiums and require specific limits.

- Storm deductibles: Separate wind or named‑storm and percentage deductibles apply in higher‑exposure areas.

- Underwriting surcharges: Wood stoves, pools, and trampolines often trigger extra liability requirements.

- Out‑of‑compliance charges: Failed roof or safety inspections may start reinspection or correction fees.

- Reinstatement and late charges: Missed payments can lead to reinstatement costs; set reminders or autopay to avoid them.

- Coverage limit adjustments: Replacement‑cost reviews can raise dwelling limits and associated premium changes.

- Nonstandard construction surcharges: Unusual roof materials or building types can increase costs; choose durable materials when possible.

How to reduce or avoid hidden fees without sacrificing coverage

Smart billing and coverage tweaks often save money while keeping needed protection intact. Start by choosing a deductible that the homeowner can pay comfortably after a claim. Then pair that deductible with annual or semiannual billing to cut installment costs. Contact Allied Insurance Agency for a free N.H. home insurance quote.

Choose the right deductible and billing cadence

Tip: A higher deductible lowers rates but should match the homeowner’s emergency budget. Using autopay or paying annually often eliminates per‑payment charges.

Bundle policies and leverage protective device discounts

Bundling auto and home policies typically reduces rates by about 14% — roughly $203–$340 a year. Document monitored alarms and safety upgrades to claim available discounts.

Proactive maintenance: roof, electrical, and plumbing updates

Keep roofs under 20 years and modernize systems to avoid reinspections and out‑of‑compliance penalties. Save invoices and photos to speed verification and limit extra costs.

Annual policy reviews to remove unneeded endorsements

Review coverage each year to remove endorsements that no longer match needs. Right‑sizing limits prevents paying for unnecessary coverage.

Compare quotes with an independent N.H. insurance agency

Compare multiple offers through an independent agent to surface lower‑cost billing options and clearer fee schedules. Ask every insurer for a detailed fee list and verify third‑party transaction charges.

- Maintain a clean claim record and improve credit to lower both rates and risk surcharges.

- Verify roof age and materials with documentation to qualify for better pricing and reduce reinspection exposure.

- Pay in full when possible to eliminate many small transaction costs and save annually.

Contact Allied Insurance Agency for a free insurance quote. For details on discounts, see New Hampshire home insurance discounts.

Reading the fine print: exclusions, limits, and NH-specific add-ons

Reading the contract line by line helps spot exclusions that raise out‑of‑pocket costs after a loss. Standard policies often exclude flood and earthquake perils. Properties near the Merrimack River in Bow, Concord, and Hooksett may carry flood risk that needs separate protection.

Common exclusions that lead to costly surprises

Flood and earthquake are generally excluded. Sewer backup and some water damage types may also be limited unless an endorsement is added.

Tip: Ask whether separate flood or specialized coverages apply to your area and request written details.

Policy limits for dwelling, personal property, and liability

Limits set the maximum payout for dwelling coverage, personal property, and liability. Replacement‑cost updates raise those limits and the price.

Review limits annually as local rebuilding costs in new hampshire areas can change quickly.

When optional coverages are worth the price in Bow, Concord, and Hooksett

Consider water backup, ordinance or law, and scheduled personal property if you have an older home or finished basement. These endorsements close common gaps.

- Confirm sublimits for valuables and schedule items when needed.

- Document upgrades to justify higher dwelling coverage at renewal.

- Read any separate wind or named‑storm deductible language carefully.

Ask for endorsements and add‑on details in writing and verify any reinspection or processing requirements before accepting changes to a policy.

Work with a New Hampshire independent insurance agency for clarity and savings

An independent agency helps residents compare multiple insurers and reveal true out‑the‑door prices. Side‑by‑side proposals make it easier to see base premium, endorsements, and any transaction charges before binding.

Why independent guidance matters in a changing market

Local advisors model how bundling, billing cadence, and deductible choices affect annual rates. Bundling often cuts costs by about 14% — roughly $203–$340 a year.

Local insight on risk, rebuilding costs, and inspection norms

An agent familiar with Concord, Bow, and Hooksett anticipates inspection triggers, roof rules, and storm exposures that shift prices. They also factor in higher local rebuild costs versus the state average premium of about $1,002 and the national $2,423 benchmark.

Contact Allied Insurance Agency for a free insurance quote.

- Compare multiple insurers to find clearer pricing and better coverage options for each home’s needs.

- Request scenarios that show how payment choices and discounts change total cost.

- Bring current policies for a no‑pressure review that aligns limits with rebuilding prices and past claims impact.

Conclusion

Summing up, knowing the full amount due — not just the quoted premium — helps residents plan and avoid surprises. A clear review highlights how credit swings, claim history, roof age, construction inflation, and local storm risk change prices and policy amounts.

Practical steps include verifying dwelling coverage limits, checking endorsements and exclusions, and documenting recent repairs to limit reinspections. Choosing the right deductible, billing cadence, and discounts can lower the cost homeowners insurance over a term.

New Hampshire’s average 2024 premium sits near $1,002 versus $2,423 nationally, but area‑level risks near rivers or in older districts can raise actual costs. Annual reviews with an independent agency let homeowners compare insurers, policies, and options to protect property and control rates.

Apply this guide to your new hampshire home decisions and seek local, independent advice tailored to your needs.

Contact Allied Insurance Agency for a free N.H. home insurance quote.