Don’t Start Another Job Without Reading This HVAC Insurance Checklist

This buyer's guide checklist helps a service owner avoid common coverage gaps before taking the next job in New Hampshire.

Contact Allied Insurance Agency in Bow, N.H. for a free hvac contractors insurance quote. This quick step can help owners, office managers, and project leads confirm the right protections and named insured details before signing a contract.

The guide explains that issuance of coverage is subject to underwriting and may not be available in all states. Policy terms, conditions, and exclusions govern outcomes. Examples here are illustrative and depend on facts and circumstances.

A fast quote is not the same as a correct quote. Clean certificates and accurate named insured data matter for getting paid and getting on site. Allied positions itself as a local resource with practical next steps for an hvac business operating in New Hampshire.

Key Takeaways

- Verify named insured and certificate details before the first job.

- Confirm policy language; exclusions can change results.

- Check that coverage fits service calls, installs, and commercial work.

- Understand underwriting limits and state availability.

- Contact Allied Insurance Agency in Bow, N.H. for a free hvac contractors insurance quote.

Why HVAC businesses in New Hampshire can’t afford coverage gaps

Service work in New Hampshire mixes property risk, worker safety, and third-party exposure on almost every call. That combination raises the chance of a claim that can derail a job or a relationship with a client in Concord or nearby towns.

Common loss scenarios on heating and air conditioning jobs

- A condensate line backs up and causes water damage to finished ceilings and floors.

- A tech drops a heavy component through a ceiling, creating costly repairs.

- A customer trips over tools and alleges injury at the work area.

What “subject to underwriting” and state availability can mean

Subject to underwriting means the insurer reviews payroll, vehicles, and scope of work before offering terms. Not all forms are available in every state, so a New Hampshire policy can differ from one issued elsewhere.

How policy language and exclusions control real claim outcomes

Limits and exclusions in the policy, not sales pitches, determine if liability or damage is covered. Contracts around Concord often require specific limits and certificate wording, so verifying documents before starting a job is essential.

How to use this buyer’s guide checklist before signing a new client

A practical, local checklist helps a company line up documents and coverage before crews mobilize in New Hampshire. The agency recommends a short, repeatable process that reduces delays and surprises.

The documents to gather for accurate quotes and clean certificates

Collect these items:

- Current policy declarations and copies of other active policies.

- Loss runs or claims history for the past five years.

- Payroll estimates and revenue by operation type.

- A vehicle list with drivers and usage details.

How to match coverage to the way they actually work in the field

Map field work: emergency service, planned maintenance, new installs, rooftop units, ductwork, and occasional subcontracting. This clarifies which operations drive exposure.

Review certificate requests carefully. Incorrect named insured, wrong addresses, or missing additional insured language can delay approvals and client access to job sites.

Set a simple handoff so the field notifies the office when a new client or scope of work is accepted. That trigger prompts an insurance review that translates real work into the correct policy structure and prevents gaps.

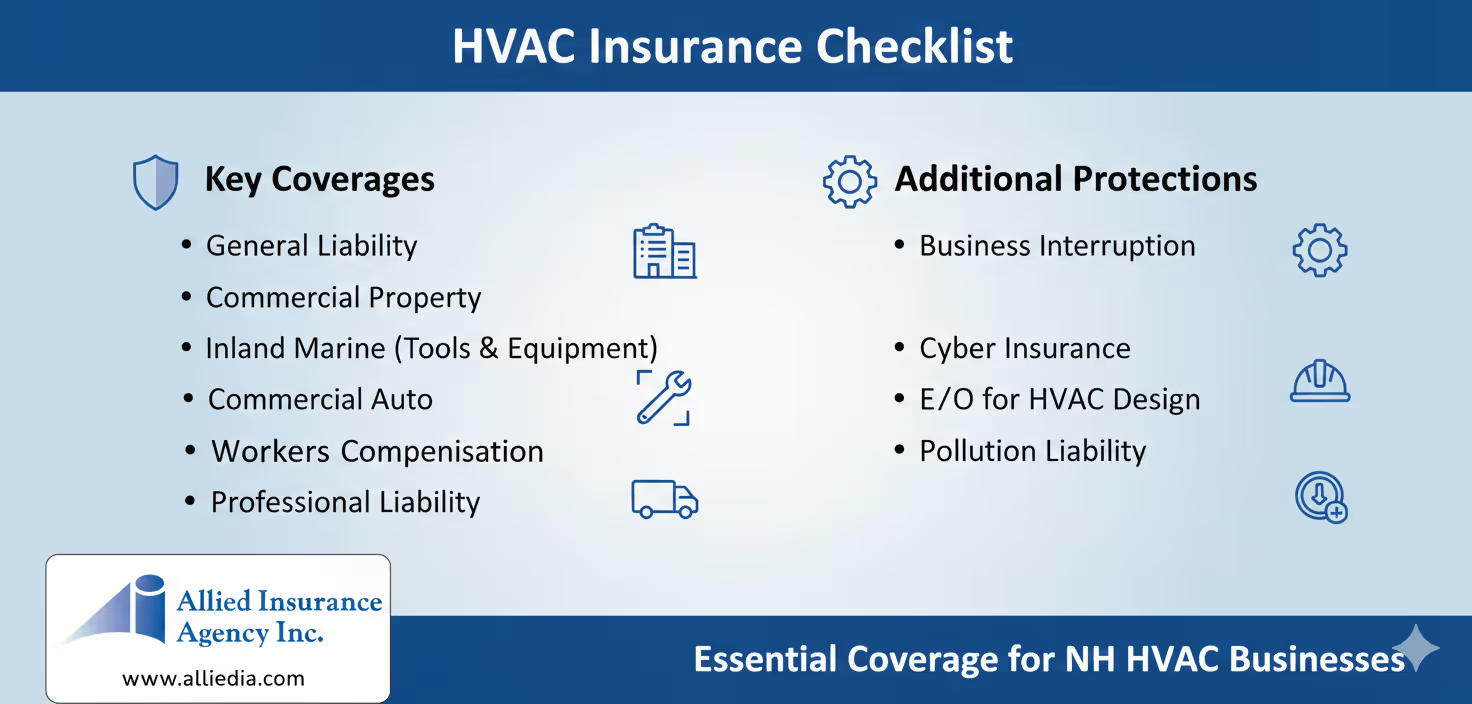

hvac contractors insurance essentials: the core policies most crews need

For New Hampshire service teams, a clear set of core policies forms the baseline for safe, contract-ready work.

General liability insurance commonly covers third-party injury and property damage that happen at a customer site. It helps when a tool falls, a pipe leaks, or property damage is alleged during a service call.

Workers’ compensation

Workers compensation responds to employee injuries and on-the-job accidents. In installation and repair work, slips, falls, and strains are common, so this coverage protects employees and the business.

Commercial auto insurance

Commercial auto insurance matters because vans and pickups act as mobile jobsites. Coverage for vehicles, tools in transit, and liability from daily driving reduces exposure on the road and between towns like Bow and Concord.

Commercial property

Property coverage typically protects the shop, office, and stored inventory. This matters in winter storms and during property damage events that affect equipment and parts kept on site.

Employer’s liability

Employer’s liability sits with workers compensation and matters when an injury becomes severe or disputed. Higher limits or an umbrella can extend general liability, commercial auto, and employer’s liability once base limits are reached.

- Core takeaway: these policies form the foundation of hvac insurance in New Hampshire.

- Next step: match limits and endorsements to contract needs and job types.

- Tip: adding the right endorsements is often as important as the base forms.

General liability insurance: what it covers and where it stops

When a customer trips in a work area or a ladder scuffs a ceiling, general liability often becomes central to the outcome.

What general liability typically covers:

- Third-party bodily injury at a residence or commercial site, such as a slip-and-fall.

- Third-party property damage from tools, ladders, or accidental impacts during a service visit.

- Legal defense and settlements for covered claims that arise from those incidents.

General liability stops short of guaranteeing the quality of a contractor’s own work. Faulty workmanship that requires repair is often excluded unless resulting damage to third-party property occurs.

Choosing limits means matching contract demands in Concord and beyond. Review client and landlord requirements, and confirm additional insured and primary wording before work starts.

Practical steps: document scope, change orders, and job photos so any liability allegation can be judged against clear records. Remember that policy language, terms, conditions, and exclusions govern claim outcomes.

Workers’ compensation in New Hampshire: protecting employees and the business

On New Hampshire job sites, employee safety and prompt medical care determine how quickly a claim is managed and costs are controlled.

How workplace injuries can happen during installation and repair

Service tasks often involve ladders, lifting heavy parts, rooftop access, and tight spaces. Strains, falls, cuts, and exposure incidents are common and can lead to time away from work.

Subcontractors, payroll, and classifications to review

Accurate payroll reporting and job classifications matter. Misclassification can trigger an audit or disputes over compensation and lead to unexpected costs for the business.

Subcontractors can create exposure if their certificate or status is not verified. Get proof before they step on site and document who is doing each task.

Return-to-work plans that help control claims costs

A simple return-to-work program helps injured employees recover while reducing long-term claim costs. Early light-duty options and clear communication speed recovery and limit disruption.

Note: Workers compensation rules vary by state and outcomes depend on policy language and claim investigations. Report incidents promptly and keep concise records.

Commercial auto for HVAC contractors: coverage for vehicles, drivers, and job duties

Regular driving between Bow, Hooksett, shops, and client sites creates real exposures for service fleets. A focused look at commercial auto helps a business control claims and costs.

Owned, hired, and non-owned exposures

Owned vehicles are those the company registers. Hired autos are rentals used for work. Non-owned autos include employee cars used on the job.

Driver selection, MVR checks, and the radius of travel affect underwriting and pricing. Document who is authorized to drive and where vehicles are garaged.

Tools and equipment inside vehicles

Auto policies often cover liability from crashes but may not protect tools and equipment left in a van or truck. For that reason, separate coverage for tools or a contractor’s equipment floater is common.

- Common claim scenarios: rear-end collisions in stop-and-go routes, parking lot damage, and injury claims from other drivers.

- Practical step: keep mileage logs, garaging addresses, and a driver roster to support cleaner certificates.

- Benefit: correct commercial auto insurance structure reduces surprises when a client requests proof of coverage.

Tools, equipment, and materials off-site: inland marine coverage that fits HVAC work

Tools and staged materials often face more risk on site than in the shop, yet many property policies do not follow them. This gap is why inland marine forms matter for local service teams in New Hampshire.

Contractor’s tools and equipment insurance

Contractor’s tools coverage protects against theft, accidental damage, and jobsite loss. It keeps crews working when a key piece of equipment is lost or broken.

Installation floater for staged materials

An installation floater covers systems, ductwork, and parts waiting to be installed. It extends protection to items at the site or in short term storage.

Transit and temporary storage

Transit coverage fills gaps when goods move from supplier to shop to job. It matters when schedules change and materials sit in vans or trailers overnight.

Real-world triggers and practical steps

- Common triggers: fire, storm damage, vandalism, and accidental loss during handling.

- Inventory tools values, update schedules, and confirm deductibles and territory.

- Remember each policy has limits and exclusions; confirm replacement valuation and claim documentation.

Builder’s risk: when the jobsite structure and materials need course of construction coverage

Builder's risk protects the physical property and materials while a structure is built or renovated in New Hampshire. It is also called course of construction coverage and applies to the structure and items staged on site.

Which projects commonly trigger this need? New builds, major renovations, and commercial tenant improvements often require builder's risk because materials sit on site before installation.

Coordinating coverage with the GC and contract requirements

Contracts frequently state who must buy the policy and who must be named. The trade should confirm limits, policy dates, and covered locations before materials arrive.

- Verify who is responsible for the policy and additional insured wording.

- Check waiver of subrogation requests so the trade does not accept terms it cannot meet.

- Document material handling and jobsite security to support underwriting and claims.

Practical step: add builder's risk to the contract checklist and share proof early. Clear roles stop finger-pointing when staged materials are damaged and help New Hampshire businesses keep projects on schedule.

For a sample contract checklist, see the contract checklist.

Commercial umbrella insurance: extra liability limits when a big claim hits

When a single large claim threatens a company’s balance sheet, extra liability limits can keep a job and the business intact.

What it does: A commercial umbrella policy steps in once underlying policy limits are exhausted. It can extend general liability, commercial auto, and employer’s liability depending on the policy schedule and terms.

When higher limits make sense

Higher limits are often needed for larger commercial accounts, municipal work, and projects with heavy foot traffic or high property values.

Practical examples:

- Third-party bodily injury at a busy site that creates large medical or legal expenses.

- Severe property damage where primary limits do not cover total loss.

- Collision claims on a company vehicle that exceed auto policy limits.

Buying and underwriting notes

Umbrella pricing can be more efficient than raising each primary policy, but it only helps if underlying coverage is placed correctly and meets umbrella requirements.

Remember: underwriting, eligibility, and claims history all affect terms. Review contractual limit requirements before bidding to avoid last-minute gaps. Umbrella protection supports steady growth, but it does not replace safe work practices and clear documentation.

Licensing and contract requirements: insurance proof, bonds, and compliance considerations

Permits and contract terms often demand more than a clean certificate; they require specific policy language. New Hampshire rules vary by state law and by town, so requirements in Concord may differ from those in smaller municipalities.

Why licensing rules and coverage needs can vary

Some towns set additional permit conditions or limits for a contractor working on public or private projects. State licensing controls baseline requirements, but local permits can add steps.

What to check in contracts and bid specs

- Required limits and the exact policy wording for additional insured status.

- Waiver of subrogation, primary and noncontributory clauses, and notice of cancellation timing.

- Any required bond amounts or certificate holder names tied to the project.

Surety bonds and the certificate process

Many permits ask for surety bonds when a permit or performance guarantee is needed. Certificates show proof but do not change the policy. Endorsements create contract-level protection.

Practical step: involve an agent early to confirm that requested terms are available and to avoid signing uninsurable contract language. The issued policy and endorsements control outcomes, not a certificate alone.

Claims readiness for HVAC contractors: what to document and how to respond fast

Clear records created at the scene make it easier to resolve disputes and support coverage decisions. A quick, organized response protects the business, the customer, and the technician. Time matters when evidence can change an outcome.

Photos, job notes, and client communications that support a claim

Collect immediately: dated photos, serial numbers, change orders, and a short timeline of what the client reported and what the technician observed. Add brief job notes and witness names.

Incident reporting basics that protect coverage decisions

Report the event to the agency promptly. Do not admit fault on site. Prompt notice preserves policy rights while allowing the insurer to start an investigation.

Coordinating repairs, mitigation, and customer expectations

Mitigate further damage quickly. Document temporary repairs and keep receipts. Communicate clearly with the client about next steps and expected timeframes.

Coverage examples are educational, not guarantees

Coverage examples are for illustrative purposes only. The policy language and claim investigation govern outcomes. Online examples help learning but do not promise a result.

- Internal process: name who calls the agency, who notifies the client, and who gathers evidence.

- Quick checklist: photos, notes, receipts, contacts, and timelines.

- Local next step: Contact Allied Insurance Agency in Bow, N.H. for a free hvac contractors insurance quote.

What drives HVAC insurance cost in New Hampshire

Understanding the pricing levers helps a service owner plan budgets without surprises. Rates reflect real business facts rather than estimates, so owners who track key inputs can forecast costs more accurately.

Payroll, revenue, and scope of work in heating and air

Payroll and revenue are primary rating bases. Higher payroll usually raises the premium because it increases exposure for workplace injuries and wage-related coverages.

Scope matters: routine service work typically rates differently than large new installations. Documenting revenue by operation type helps underwriters set a fair cost.

Vehicles, radius, and driving exposure from Bow to Hooksett

Vehicle counts, how far crews drive, and daily routes influence auto and liability pricing. Longer radiuses and more vans increase frequency exposure and can raise the cost.

Garaging addresses and driver histories also matter. Clear records of authorized drivers and miles reduce surprises at renewal.

Claims history, deductibles, and selected policy limits

A clean claims history lowers rates while past losses push rates higher. Choosing higher deductibles usually reduces premium but raises the business's retained cost if a claim occurs.

Selected limits affect both premium and risk. Matching limits to contract demands prevents costly retrofits later.

Tools values, jobsite security, and material handling

Declared values for tools and equipment feed property and inland marine pricing. Strong jobsite security and documented handling procedures can reduce theft and loss frequency, which helps costs over time.

- Underwriting reality: each applicant is reviewed individually; rates and discounts vary by facts submitted.

- Practical step: inform the agent when new services, locations, or vehicles are added so the policy stays aligned and renewals go smoothly.

How to compare policies and quotes without missing hidden gaps

Comparing quotes takes more than price; it requires a side-by-side look at what a policy actually promises. An independent New Hampshire agent can show differences clearly and point out local nuances that affect coverage.

Match limits, deductibles, and endorsements apples-to-apples

Compare limits and deductibles using the same claim scenarios. Note per-occurrence and aggregate limits, and list deductibles for each exposure.

Check exclusions that commonly impact contractors

Watch exclusions closely. A single exclusion can remove needed coverage for completed operations, tools, or transit. Ask the agent which endorsements restore protection.

Confirm who is insured: entities, additional insureds, and workers

- Verify the legal entity and any DBA names on the policy.

- Confirm additional insured wording and waiver of subrogation when a client requests it.

- Check classifications, payroll assumptions, and vehicle schedules so workers and operations are included.

Practical step: document differences, ask for plain language explanations, and keep the chosen comparison in writing. Remember that policy language governs and that coverage can vary by state before binding.

Working with an independent New Hampshire insurance agency: local guidance for Bow, Concord, and Hooksett

An independent New Hampshire agency translates contract language into practical coverage advice. They help a hvac business align real work with proper policy terms. Local agents see seasonal risks and town permit quirks that national forms miss.

Building a coverage plan that fits service work, installs, and commercial projects

The agent crafts plans to match daily service calls, new installs, and larger commercial projects. This avoids one-size-fits-all gaps. A tailored plan keeps the crew moving and reduces claim surprises.

Certificates, contract review support, and keeping policies current

Agents review certificate wording, additional insured requests, and waiver language before crews arrive. They can prepare endorsements and confirm that coverage meets a client or landlord requirement.

When to revisit coverage as the company adds employees and vehicles

- Update payroll and roles when new employees join.

- Add vehicles and driver details as fleet size grows.

- Recheck coverage for subcontracting and larger staged material values.

Practical partner: the agency answers “Does this contract requirement match the policy?” and “Will this jobsite exposure be covered?” Contact Allied Insurance Agency in Bow, N.H. for a free hvac contractors insurance quote.

Conclusion

A solid coverage plan starts with mapping real job risks and matching them to policy terms.

This checklist reminds teams in New Hampshire to align liability, workers compensation, auto, property, and off-site tools and equipment protection with how they actually work.

Keep clear photos, short job notes, and communication logs so claims get resolved faster. Compare quotes by reading policy language, not just price, because exclusions and underwriting control outcomes.

Revisit limits after hires, added vehicles, or bigger commercial work. Coverage availability is subject to underwriting and may vary by state, and the issued policy governs terms and exclusions.

Next step: Contact Allied Insurance Agency in Bow, N.H. for a free hvac contractors insurance quote.